Accelerate Monthly:

Diversify Your Bonds

October 12, 2022 — For most of 2020, the 10-year Treasury yield hovered below 1.0%.

“You would lend money for 10 years at an interest rate of less than 1%?” I would ask allocators. “Why?”

Even though the yield was unappealing to most, if not all investors, those holding long-term Treasury bonds did so under the guise of an insurance policy.

“They are there to protect the portfolio when stocks go down,” they said.

Unfortunately, the thesis did not play out, and now both stocks and bonds are down markedly.

In fact, performance in 2022 is in line with one of the worst years on record for the traditional 60% stock / 40% bond portfolio.

However, compared to 2008, which featured a similar plunge for the traditional portfolio, one could argue that 2022 is markedly worse.

During the global financial crisis fourteen years ago, stocks plummeted, however, Government bonds rallied, acting as a portfolio cushion and providing some solace to decimated equity positions.

This year, Government bonds’ insurance policy stopped working as bonds tanked, with low starting yields and surging inflation the culprit.

U.S. Treasury bonds are suffering their worst drawdown in recent history. Who would have thought the “safe” asset would drop more than -15%? Previous drawdowns were rarely more than -6%.

A new approach to asset allocation is needed.

Why?

The fallacy of the 60/40 stock/bond portfolio is that bonds are negatively correlated with stocks. That is, bonds go up when stocks go down. This fallacy was reinforced by the previous three bear markets (2001, 2008, and 2020), in which bonds experienced positive performance as equities fell.

However, empirical data show that throughout most of the past 70 years, stocks and bonds were positively correlated.

Stocks and bonds are moving in the same direction this year and both losing money is a return to normal after an abnormal two decades in which they were negatively correlated.

Evidence shows that bonds do not diversify a stock portfolio as previously thought.

Reflecting on current allocations, I hear many investors say, “Stocks and bonds are down so much, they offer great potential returns from here.”

However, on a go-forward basis, the 60/40 portfolio offers a prospective long-term real return of just 3% per annum.

Currently, the Canadian bond index yields 4.3%, while the U.S. bond index yields 4.7%. If we assume inflation goes back to 2% over the next few years (a big if!), then bonds would yield an expected 2.3% to 2.7% on a real (inflation-adjusted) basis.

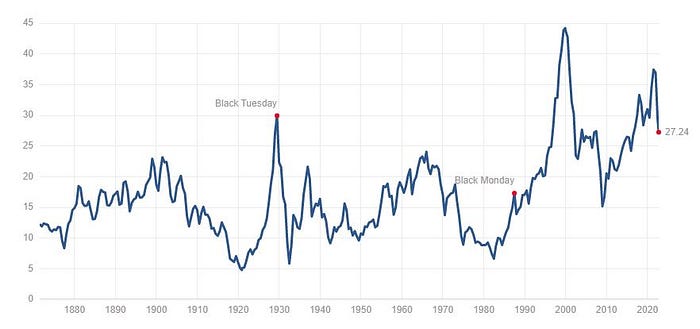

While cyclically-adjusted U.S. equity valuations have dropped from 40x to 27x, they are still 60% above their long-term average valuation of 17x.

Source: Multipl.com

Similar to how a bond’s beginning interest rate yield is the best indicator of long-term return, a stock’s beginning earnings yield (i.e. valuation) is the best predictor of its future expected return.

The data show that forward equity returns are related to current stock market valuations.

The higher the stock market’s valuation, the lower the future return.

With the U.S. stock market at 27x cyclically-adjusted earnings, we can expect a future long-term annualized return of 3.0% above inflation (or 5.0% nominal assuming a 2.0% future inflation rate).

Canadian stocks are trading at 20x cyclically-adjusted earnings, equating to an expected real return of 5.3%.

Therefore, with U.S. bonds expected to return 2.7% per annum and U.S. stocks to generate 3.0% annually (inflation-adjusted), the U.S. 60/40 portfolio is expected to produce a 2.9% real return annually on a go-forward basis.

The Canadian 60/40 portfolio has a slightly higher forecast real return of 4.1% (60% x 5.3% + 40% x 2.3%).

Even after a challenging year in 2022, the traditional 60/40 portfolio presents below-average expected future returns.

Given the two core ideas above, including the lack of diversification between stocks and bonds and with their low expected future returns, it is only logical to consider alternative asset classes in search of both returns and diversification.

We posit arbitrage as an alternative fixed-income allocation:

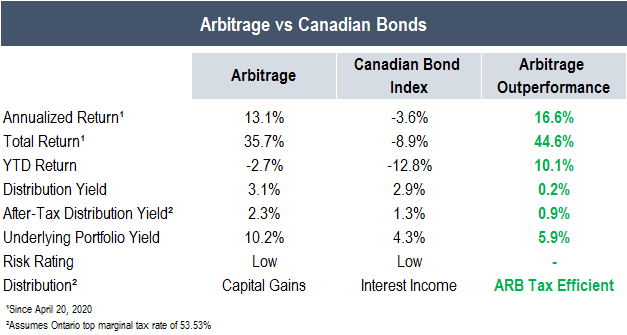

Source: Accelerate, iShares

Since we launched the Accelerate Arbitrage Fund ETF (TSX: ARB) nearly three years ago, it has outperformed the Canadian bond index by approximately 45.0%, or 16.6% annualized. ARB is outperforming bonds by more than 10.0% year-to-date, cushioning investor portfolios from double-digit losses through diversification. In addition, ARB has a higher distribution yield, amplified on an after-tax basis given arbitrage’s tax efficiency (it generates yield via capital gains as opposed to interest income from bonds). Moreover, with arbitrage spreads at their widest in years, ARB has a higher expected return compared to the Canadian bond index, given ARB’s underlying yield of over 10.0% versus the 4.3% underlying yield from the bond index.

If one is looking to diversify their bond portfolio, which is logical given bonds’ expected return and correlation dynamics, then arbitrage may be a good pick.

Accelerate manages five alternative ETFs, each with a specific mandate:

- Accelerate Arbitrage Fund (TSX: ARB): SPAC and merger arbitrage

- Accelerate Absolute Return Hedge Fund (TSX: HDGE): Long-short equity

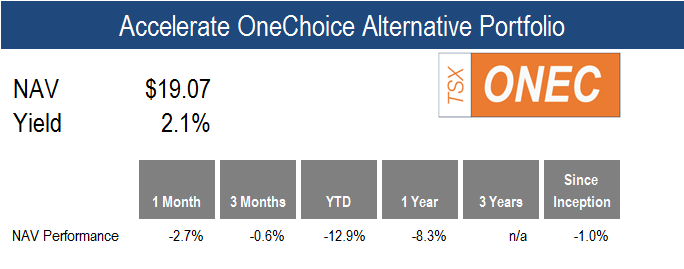

- Accelerate OneChoice Alternative Portfolio ETF (TSX; ONEC): Alternatives portfolio solution

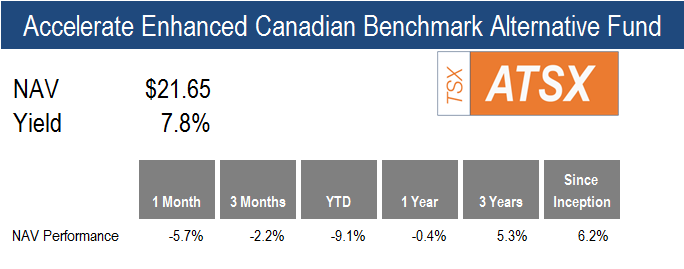

- Accelerate Enhanced Canadian Benchmark Alternative Fund (TSX: ATSX): Buffered index

- Accelerate Carbon-Negative Bitcoin ETF (TSX: ABTC): Eco-friendly bitcoin

Please see below for fund performance and manager commentary.

ARB fell -0.4% in September, as spreads widened across the board.

Throughout the month, merger arbitrage yields rose from 11.4% to 14.4% while SPAC arbitrage yields rose from 5.6% to 5.9%. Prices fall as yields rise.

The rise in arbitrage yields resulted from the surge in Treasury yields, which increased funding costs. Arbitrage yields rising was not due to an increase in risk premiums.

Specifically, the 2-year Treasury yield rose from 3.5% to 4.3%, while junk bond yields went from 8.4% to 9.7%.

Twelve M&A deals worth an aggregate $32 billion, closed during the month, including Vista Equity Partners’ massive $16.5 billion leveraged buyout of Citrix Systems. This deal had previously caused consternation in the market, given its copious amount of leverage amid shaky stock and bond markets, but ultimately closed on the terms. Deals closing as expected is constructive for merger arbitrage in general, but equity market volatility and rapidly rising rates have led to the widening of arbitrage spreads. In any event, despite the market turbulence, we expect deal completion rates in line with historical averages.

Despite the SPAC market shrinking from $200 billion to $160 billion year-to-date, it still offers $2.6 billion of aggregate arbitrage profit.

One of the main benefits of arbitrage is its low duration, which allowed it to outperform other fixed-income asset classes markedly in 2022. Specifically, the average SPAC has 4.8 months to maturity, while the average merger has a duration of just 2.7 months.

HDGE fell -3.9% in September as multi-factor performance was mixed. Particularly, all U.S. long-short factors generated alpha across the board, but nearly all Canadian long-short factor portfolios experienced negative performance.

The U.S. long-short multifactor portfolio gained 7.1%, as the long portfolio’s -9.0% decline was more than offset by the short portfolio’s -16.1% drop. Each long-short factor, including value, quality, price momentum, operating momentum, and trend, generated outperformance during the month. However, each U.S. long factor portfolio dropped between -7.7% and -9.6%, while each short factor portfolio returned between -13.3% and -16.2%.

Since HDGE is a systematic hedged strategy that rebalances to approximately 110% long and 50% short each month, the declines in the plummeting short portfolio were not enough to fully offset the negative performance of the long portfolio.

In a challenging environment for risk assets during a month in which the S&P 500 dropped -9.2%, ONEC fell -2.7% as most asset classes suffered declines.

Only one alternative strategy was in the green, with the Canadian mortgage portfolio up just +0.1%. Arbitrage limited the Fund’s losses at -0.4%.

The alternative currencies, gold and bitcoin, fell less than -3%. Long-short equity, leverage loans and the U.S. mortgage portfolio were down between -3% and -5%. Alternative equity was down -5.7%

The biggest detractors for the month came from the real assets and global macro buckets. Specifically, the real estate portfolio was down -8.3% while the infrastructure portfolio dropped -9.4%. Risk parity was the bottom performer, falling by -11.5%.

ATSX returned -5.7% for the month, underperforming the benchmark TSX 60’s -3.9% decline.

ATSX’s long-short overlay portfolio detracted -1.8% from the September portfolio performance.

Canadian multi-factor portfolios underperformed during the month, with the long-short multifactor portfolio dropping -4.9%. The value, quality and trend long-short factors dragged on performance with declines of -2.5%, -3.5%, and -3.5%, respectively.

September’s underperformance narrowed ATSX’s lead over the TSX 60 to 150bps year-to-date.

Have questions about Accelerate’s investment strategies? Click below to book a call with me:

-Julian

Disclaimer: This distribution does not constitute investment, legal or tax advice. Data provided in this distribution should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this distribution is based on current market conditions and may fluctuate and change in the future. No representation or warranty, expressed or implied, is made on behalf of Accelerate Financial Technologies Inc. (“Accelerate”) as to the accuracy or completeness of the information contained herein. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Past performance is not indicative of future results. Visit www.AccelerateShares.com for more information.