Accelerate Monthly -

Speculators Gone Wild

March 10, 2024 — A generation ago for today’s market participants, the late 1990s featured a historic stock market bubble concentrated in technology and telecom stocks. The dot-com bubble, as we now call it, was driven by a “new economy” thinking that a hot emerging technology, the internet, would change society, commerce, and investing forever.

The internet certainly changed everything, however, most internet-related investments resulted in a complete loss for investors. As a result of the bubble, speculative activity and animal spirits allowed for a tremendous misallocation of capital, with disastrous results for many of the investment opportunities at the time. While the tech bubble created some significant winners, such as Amazon.com, even the stocks that went on to do the best over the subsequent decades were available at prices 50% to 95% lower after the bubble burst.

Alan Greenspan, the Chairman of the Federal Reserve at the time, is famously associated with coining the term “irrational exuberance” during a speech in December 1996, which many interpreted as a warning that the stock market was overvalued. Despite this, the market continued its rapid ascent over the next several years until it peaked in March 2000 and subsequently crashed. The bursting of the dot-com bubble had a particularly nasty effect on the global economy, causing an economic recession that wiped the speculative excesses and capital allocation mistakes of the bull market from the system.

Greenspan’s Federal Reserve took steps to manage the situation by adjusting interest rates. For instance, in response to the collapse of the hedge fund Long-Term Capital Management in 1998, which was a significant event at the time due to the firm’s extensive use of leverage, the Federal Reserve under Greenspan organized a bailout and also lowered interest rates in an attempt to stabilize the market. These interest rate cuts were part of a broader policy strategy, often criticized in hindsight, that may have contributed to the forming of the stock market bubble.

Additionally, after the dot-com bubble burst, the Greenspan Fed lowered interest rates to mitigate its impact on the economy. While this action helped in the short term, some argue that it laid the groundwork for the housing bubble and the subsequent financial crisis in 2008 by making borrowing cheaper and thus encouraging an increase in housing prices and mortgage lending.

In general, the Federal Reserve under Greenspan has been both praised and criticized for its actions during the late 1990s and early 2000s. The critique often focuses on the Fed’s easy approach to monetary policy, which was characterized by lowering interest rates in response to financial crises, potentially fostering an environment conducive to risk-taking and contributing to subsequent asset bubbles.

Nonetheless, it is worthwhile for investors and Fed-watchers alike to consider the lessons learned by central bankers from the last major stock market bubble and the effect of Fed Policy, or lack thereof, in influencing how large the bubble grew and how painful the subsequent popping was for both investors and the economy.

Is the Bubble Back?

The “new era” thinking caused by the emergence of the internet in the late 1990s is almost perfectly analogous to the current sentiment around artificial intelligence. What was the previous generation’s bubble dot com might be this generation of investors’ bubble dot AI.

Whether the current market is classified as a bubble, which tends to be only discernable with the benefit of hindsight, investors should note the alarming signs and red flags regarding U.S. large-cap growth stocks and other risky assets. Certain red flags in the market indicate a highly speculative trading environment reminiscent of the late 1990s and 2021.

Over the past six months, financial conditions have eased materially, and are back to levels last seen during the market frenzy of 2021. This dramatic easing of financial conditions has occurred before the Fed even commenced a much-anticipated rate-cutting cycle. If the current market is in fact overheated, central bank rate cuts could be comparable to throwing gasoline on an out-of-control grassfire.

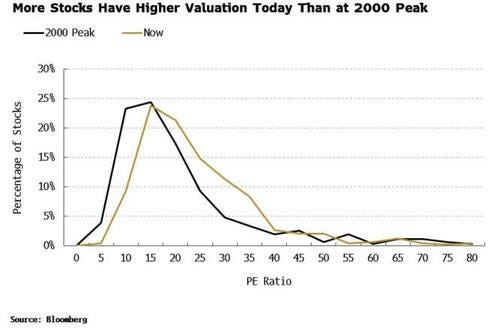

A loosening of financial conditions has caused a boom in risk assets, markedly lifting the valuations of equities. Nearly 25% of the U.S. equity market is now valued north of 10x revenue, nearing peak levels of 28% in 2021 and 35% at the nadir of the tech bubble in 2000. For U.S. large-cap growth stocks, valuations are well into nosebleed territory.

Based on earnings, the U.S. stock market features a larger percentage of companies trading at higher valuations than at the peak of the tech bubble. There are no ifs, ands, or buts about it — stocks are expensive.

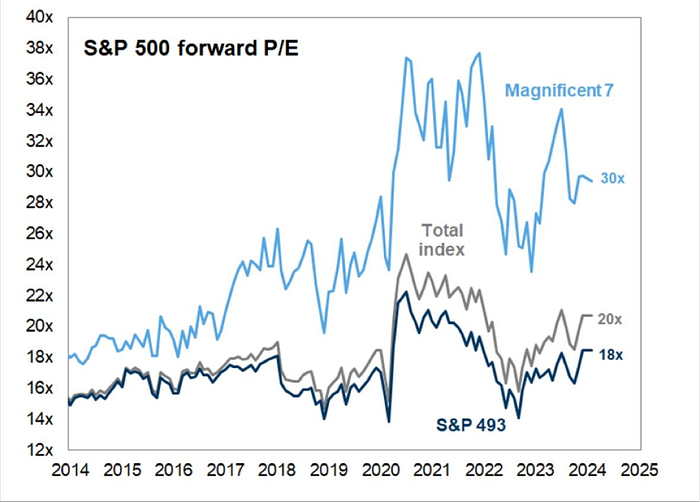

While the S&P 500 trades at a stretched valuation above 20x next year’s earnings, much of the substantial increase in valuations has been driven by the Magnificent 7 stocks, including Apple, Microsoft, Alphabet, Amazon.com, Nvidia, Tesla, and Meta Platforms.

As the S&P 500’s valuation has risen from 15x to 20x earnings over the past decade, the Magnificent 7’s earnings multiple has surged from 18x to 30x, now dominating the benchmark index.

Typically, market participants ascribe higher earnings multiples to faster-growing companies. This sentiment makes sense, as multiples are short-hand valuation techniques for a discounted cash flow analysis (DCF). In a DCF model, the faster the earnings growth, the greater the present value of future cash flows and the more valuable an asset.

Oddly, we have seen valuations surge while revenue growth of the large-cap tech stocks has completely stalled. Since peaking in early 2022, the tech sector’s annual revenue growth has declined from a scorching-fast rate of 16% to a moribund negative growth rate currently.

If it is not fundamentals driving equity performance, something else must be at play. As artificial intelligence applications become more prevalent in our lives, and this emerging technology becomes more consequential, investors equate generative AI use cases + clicks = stock market riches. Given the productivity enhancements that AI has the potential to bring, extreme bullishness on the sector is understandable (this coming from one of the biggest advocates of AI).

The publicly-traded poster child for the AI revolution, Nvidia, is up 82% year-to-date and 273% over the last 12 months. Its exceptional stock market performance has been driven by providing this new economy’s picks and shovels. Nvidia’s GPUs are in massive demand from the Magnificent 6 (the Mag7 less Nvidia), as these tech giants build out their generative artificial intelligence capabilities. It is a gold rush, and Nvidia is selling as many chips as it can produce at enormous margins, with more than half of its revenue coming from the Magnificent 7 less 1. Now that the market has priced in continued robust growth in AI spending, manifested through well-above-average valuations and high expectations, the critical question for investors is how sustainable the current level of expenditures on AI infrastructure is and the commercial potential of (profitable) generative AI use cases.

It is fair to pushback on why investors should care about high valuations. The economy is doing fine, inflation is coming down, the Fed will start cutting interest rates, and AI will change the world. Aren’t those factors sufficient to justify near record-high stock valuations?

The reality of the situation is that valuations drive future returns. According to the analysts at Bank of America, the S&P 500’s current valuation implies a 3% annualized return for the benchmark index over the next decade. Most investors will likely be disappointed with that performance.

Source: BofA

That being said, forecasts are not guaranteed, and for now, the S&P 500 and Nasdaq 100 indexes are reaching new all-time highs seemingly every day. Animal spirits are out in full force, and most investors do not want to miss out on the market spoils that AI will bring. As long as share price charts are up and to the right, who cares about valuations, analysis, or forecasts?

Source: X

Nevertheless, the market’s AI-fueled animal spirits are out in full force across speculative asset classes beyond merely large-cap growth stocks. Nvidia’s more than $1 trillion in market capitalization growth over the past year has spread to other stocks and asset classes.

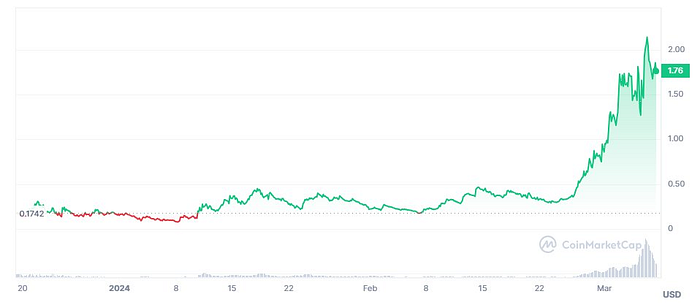

If you don’t believe that speculative excesses are at least a little overheated, note that a dog memecoin called dogwifhat, a cryptocurrency with no use case created just three months ago, has surged 1,000% to a $1.8 billion market capitalization. If you have lost track, dogwifhat is at least the third dog-themed memecoin, after Dogecoin ($24 billion market cap) and Shiba Inu coin ($21 billion market cap).

Source: Coinmarketcap

This speculation is but one of thousands of examples occurring in the current market environment.

While markets are no strangers to pockets of speculative excesses, the current frenzy appears relatively broad-based. So much of the market has been infiltrated by Reddit-style YOLO investing that it would be downright irresponsible if central bankers were not paying close attention.

Fed policy is dramatically impacted by historical events, and taking a page from the tech bubble, central bankers may worry that adding fuel to the fire of a speculative fervour via interest rate cuts may be comparable to Greenspan’s heavily criticized easy money policies that appear to have fuelled two previous bubbles (stocks in the 1990s and housing in the 2000s). It is not out of the question for central bankers to pull back on potential rate cuts due to rampant asset price inflation and irrational exuberance in equity, crypto, and other markets.

Central bankers would be justified in seeking to dampen, rather than fuel, broad-based asset price bubbles because the real-world economic consequences can be devastating. After the last two Fed-fueled bubbles popped in 2000 and 2008, respectively, the resulting deep recessions and associated job losses took several years to recover from. When bubbles burst, the unwind can be ugly, as selling begets selling, triggering a cascading effect.

The effects of a bubble unwinding usually spread to other sectors or markets, especially if the bubble is in a critical sector of the economy. This contagion can exacerbate the economic impact, with unknown consequences. Financial institutions usually experience losses from the unwinding of the bubble, leading to the tightening of credit conditions. This results in a credit crunch, where businesses and consumers find it more difficult to borrow money, causing a marked slowdown in economic activity. As they say, the bigger they are, the harder they fall.

With speculation running rampant, equity valuations reaching nosebleed levels, and recent Fed communication driving a dramatic easing of financial conditions, the drumbeat for the justification of zero interest rate cuts in 2024 grows louder. Widespread irrational exuberance, along with the desire not to repeat previous policy mistakes, provides the Fed with sufficient cover to maintain a tighter monetary policy stance in the face of both market and political pressure.

Whatever happens with respect to monetary policy, investors should be at least a bit fearful when others are greedy. Incorporating downside protection in investment portfolios could prove prescient.

Accelerate manages four alternative ETFs, each with a specific mandate:

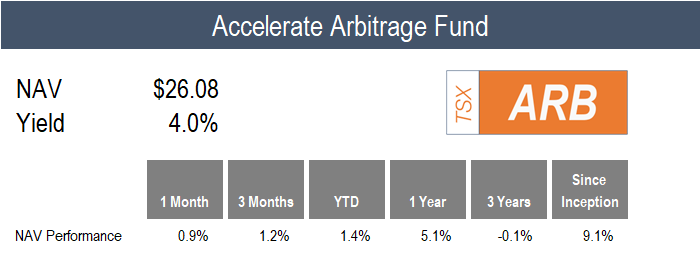

- Accelerate Arbitrage Fund (TSX: ARB): Cash Plus

- Accelerate Absolute Return Hedge Fund (TSX: HDGE): Portfolio Protector

- Accelerate OneChoice Alternative Portfolio ETF (TSX: ONEC): Portfolio Stabilizer

- Accelerate Enhanced Canadian Benchmark Alternative Fund (TSX: ATSX): Canadian 150/50

Please see below for fund performance and manager commentary.

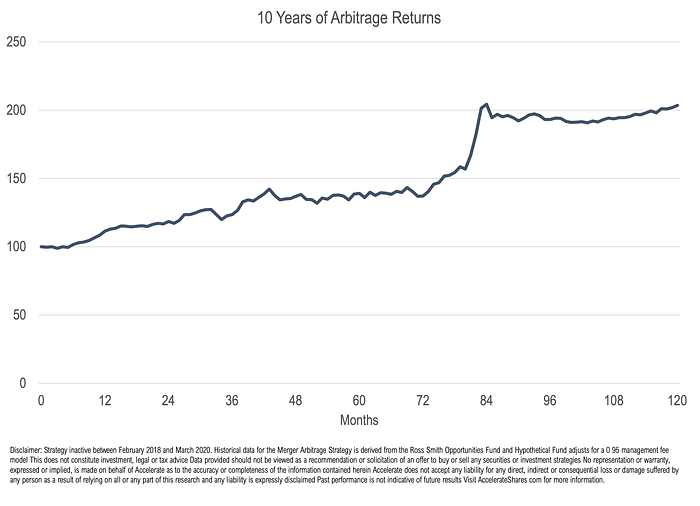

ARB gained 0.9% in February, compared to a 0.3% return for the S&P Merger Arbitrage Index.

Over the past couple of years, we lamented that overbids and bidding wars were few and far between, occurring at rates well below the historical average.

Historically, approximately 5% of mergers were subject to an increased consideration, either through a bidding war spurred on by an interloper or the original bidder being forced to pay a higher price.

The drought ended last month, as ARB was the beneficiary of the overbid for Osino Resources, a gold exploration and development company with a project in Namibia. In December, Osino struck a friendly merger with Dundee Precious Metals at $1.56 per share. A couple of weeks ago, interloper Yintai Gold came over the top with a $1.90 cash bid, besting Dundee’s price by 33%, resulting in a nice bonus and the crystallization of upside optionality for arbitrageurs.

It was a relatively active month for merger activity, with 17 deals announced representing an aggregate value of nearly $80 billion. ARB established four new arbitrage investments, with a focus on leveraged buyouts and biotech mergers.

The Fund remains fully invested, with gross exposure of 149.8%, consisting of 137.2% long and -12.6% short. The portfolio is allocated 53% to SPAC arbitrage and 47% to merger arbitrage, consisting of 13% to LBOs and 34% to strategic M&A.

February was a notable month; in that it was the 120th month I have professionally managed a merger arbitrage hedge fund. Over these 10 years (including more than 6 years as a private fund and nearly 4 years as an ETF), we conducted a detailed analysis of 4,094 M&A deals and invested in approximately one-quarter of them.

Let’s hope the next 10 years are as fruitful as the past 10.

HDGE generated a 6.5% return for the month, bringing its year-to-date return to 14.2% and its 3-year annualized return to 21.9% per annum. The Fund will hit its 5-year anniversary in two months.

February was somewhat challenging to navigate. While multifactor long-short portfolios produced mostly positive returns during the month, save for long-short value in the U.S., the current speculative market dynamics made short selling fraught with risk. For example, the Goldman Sachs Most Shorted Index surged 16.6% last month, with overvalued junk stocks leading the way. The Fund’s robust short portfolio risk models have paid dividends for the Fund, particularly when the market gets “squeezy”.

Nevertheless, the current environment remains beneficial for the Fund. Higher interest rates, which lead to attractive returns on cash generated by the Fund’s short portfolio, and wide stock dispersion, with a significant number of overvalued junk stocks outstanding, have created unique tailwinds for absolute return.

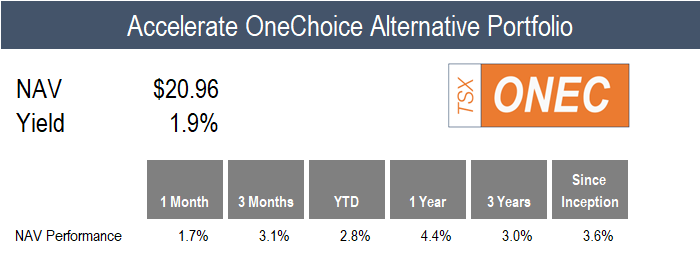

ONEC generated a 1.7% return in February, a relatively consistent month for alternative asset classes.

The hedge fund allocations contributed positively overall to the Fund’s monthly return. Specifically, absolute return led the pack with a 6.5% gain, followed by a 3.7% return from managed futures, and 1.3% and 0.9% from long-short equity and arbitrage, respectively. Risk parity contributed negatively, falling -0.4%.

Real assets continued to trend higher, with infrastructure gaining 0.8% and the real estate portfolio adding 2.1%.

The credit allocation, consisting of leveraged loans and mortgages, and the inflation protection bucket, consisting of gold and commodities, were flat for the month.

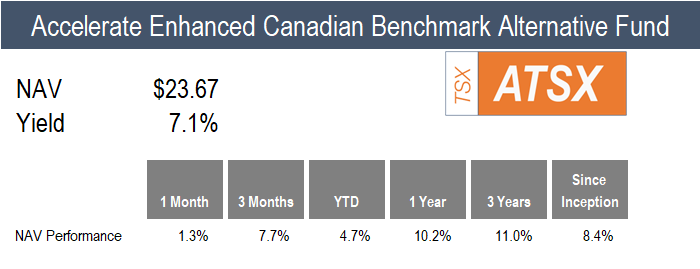

Canadian long-short factor performance was positive across the board in February, leading to a 1.3% gain for ATSX compared to a 2.0% gain for the benchmark TSX 60 Index.

The trend and price momentum factors led the Canadian long-short portfolios for the month, gaining 6.0% and 5.1%, respectively. The quality and value market-neutral portfolios were up 5.1% and 4.0%, while long-short operating momentum ticked up 2.6%.

Have questions about Accelerate’s investment strategies? Click below to book a call with me:

-Julian

Disclaimer: This distribution does not constitute investment, legal or tax advice. Data provided in this distribution should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this distribution is based on current market conditions and may fluctuate and change in the future. No representation or warranty, expressed or implied, is made on behalf of Accelerate Financial Technologies Inc. (“Accelerate”) as to the accuracy or completeness of the information contained herein. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Past performance is not indicative of future results. Visit www.AccelerateShares.com for more information.