Cash Plus: The Ultimate Upgrade to Cash for Enhanced Returns

May 30, 2023 — On November 9, 1993, legendary hip hop group Wu-Tang Clan released the song “C.R.E.A.M.”, an acronym for Cash Rules Everything Around Me. The song featured verses from several Wu-Tang members, who discuss their upbringings while living in New York City.

While Raekwon, Inspectah Deck, and Method Man did not explicitly state they were buying short-term T-bills when they rapped “cash rules”, with short-term Treasury bills yielding approximately 3.0% at the time, its message resonated with both hip-hop fans and investors alike.

Source: Bloomberg

Cash as an investment strategy fell out of favour from 2009 to 2021, as cash yields dropped to near 0%. However, the song has remained relevant over the past thirty years. In 2011, Time magazine included C.R.E.A.M on its list of All-Time 100 Greatest Songs.

When short-term T-bills offer attractive yields, cash rules everything around investors. And with the short-term cash yields of 5.2% available today, cash allocations are ruling investors’ asset allocation decisions.

While a 5.2% return with nil risk is appealing, especially with the inflation rate sporting a 4-handle in North America, it is always worthwhile asking, “Can we do better?”

In our May 2020 memo, The Art Of SPAC Arbitrage, we detailed how a Special Purpose Acquisition Company may function as a T-bill equivalent:

“The key aspect of SPAC arbitrage is the existence of untouched capital from the IPO invested in risk-free U.S. government securities, giving investors a baseline return of short-term treasury yields, combined with a set deadline offering the ability to redeem shares for the underlying net asset value (NAV, or the value of the treasuries plus accrued interest) either around the date of the vote for the SPAC’s business combination or its liquidation date.”

A pre-deal SPAC can be considered a redeemable T-bill plus an equity call option. Depending on its price, a SPAC can trade at a discount, or a premium, to its underlying net asset value. The call option aspect of the equation refers to the notion that a SPAC can trade above its redeemable NAV upon announcing a business combination that the market deems to be attractive.

A pre-deal SPAC trading at a discount to NAV is analogous to a discounted T-bill plus an equity call option. For example, a SPAC trading at $10.30 with a $10.50 NAV represents a T-bill trading at 98 cents on the dollar. This discounted T-bill offers a premium yield — what we call “cash plus”.

A cash plus investment strategy enjoys certain advantages over a plain vanilla T-bill or a high-interest savings account.

SPACs trading below NAV offer two unique advantages over cash strategies in particular:

- Higher yields: The ability to earn yields above cash given the discounted price.

- Tax efficiency: The ability to earn yield via capital gains instead of interest income.

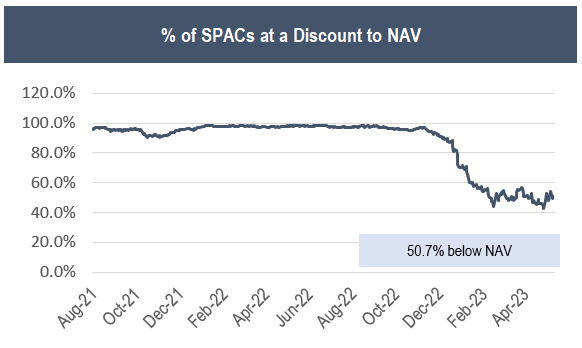

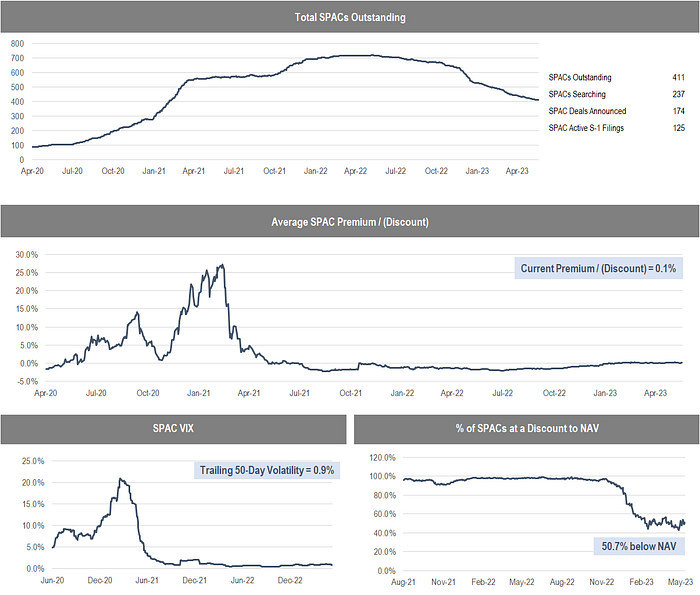

For an investor looking for cash plus opportunities in SPACs, 410 redeemable blank check companies are listed, and more than half are trading at a discount to NAV.

Source: Accelerate

There are currently 57 blank check companies with a duration longer than 30 days trading at yields above 5.3%, representing an aggregate value of $3.6 billion.

The SPAC market remains dynamic, with new yield opportunities for enterprising investors offered on a daily basis. New issuance remains slow but relatively steady, with three new blank check IPOs in May, representing $407 million in total. The Accelerate Arbitrage Fund (TSX: ARB) participated in all three SPAC IPOs issued this month.

New issuance can offer an attractive place for yield-focused investors to look. In our March memo, IPO: It’s Potentially An Opportunity, we discussed how investors might be able to generate an upfront expected yield from a SPAC IPO of 6.0% to 10.0%.

While new SPACs continue to be issued each month, the market is still shrinking as far more blank check vehicles are maturing. In May, twenty-one matured, with seventeen liquidating and four conducting a business combination. As the market-right sizes, we expect fewer liquidations as a percentage of total maturations, allowing for SPAC warrants and rights to crystalize more value for investors.

In any event, one benefit of SPAC arbitrage is that we get paid to wait, and the higher short-term Treasury yields go, the more we get paid. And while cash still rules given current yields on cash offered, SPAC arbitrage may represent a more attractive cash plus strategy given its higher potential yield over T-bills and high-interest savings accounts and its tax efficiency of yield via capital gains. It is not quite a remix of the classic track (and investment strategy) C.R.E.A.M., but perhaps an upgrade.

The Accelerate AlphaRank SPAC Monitor details various metrics on the current opportunity set while offering details on every individual SPAC currently outstanding. The Accelerate AlphaRank SPAC Effective Yield tracks the average arbitrage yield offered. The Accelerate AlphaRank SPAC Index tracks the price return of the SPAC universe.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). The Accelerate Arbitrage Fund may hold a number of securities discussed in this research. Visit AccelerateShares.com for more information.

Disclaimer: This research does not constitute investment, legal or tax advice. Data provided in this research should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this research is based on current market conditions and may fluctuate and change in the future. No representation or warranty, expressed or implied, is made on behalf of Accelerate as to the accuracy or completeness of the information contained herein. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Accelerate may have positions in securities mentioned. Past performance is not indicative of future results.