M&A Revolution: Riding the Wave of Consolidation

May 28, 2023 — “Sell in May and go away” goes the old Wall Street adage.

For those who abide by this mantra, hopefully, they did not sell their Nvidia stock (up more than 40% this month!).

The origins of this saying can be traced back to the historical patterns previously observed in stock market returns. Historically, there has been a seasonal pattern in stock market performance where the market tends to experience lower returns on average during the summer months, particularly from May to October.

The rationale behind the stock market trading strategy of selling prior to the summer doldrums is rooted in a combination of factors, including reduced trading volumes during the summer months, lower investor participation due to vacations, and historical underperformance of certain sectors during this period. In addition, some argue that economic and market conditions, such as corporate earnings releases, political developments, or policy decisions, tend to have a relatively lower impact on the market during the summer months.

Nevertheless, from the perspective of the merger arbitrageur, who seeks to generate absolute returns that are uncorrelated with the stock market, whether stocks go up or down is largely irrelevant.

What matters is deal flow.

Does the same summer slowdown that has historically influenced stock market returns have the same effect on mergers and acquisitions activity?

The data show that while sell-side investment bankers and target company corporate executives are selling (companies) in May, as it is generally a busy month for M&A, merger specialists typically stay active throughout the summer as the deal flow continues throughout June, July, and August. Historically, there has been no discernable summer doldrums in the M&A market.

This year is no different. In fact, May 2023 featured the highest number of announced U.S. public mergers and acquisitions since November 2021. Merger arbitrageurs are very busy these days.

Source: Accelerate

The current wave of consolidation picked up markedly this month, with 69% more deals announced this month than the average from January through April.

Given the excess supply of deals and insufficient arbitrage capital to account for the substantial increase in mergers, risk premia are high and merger arbitrage yields are attractive.

Source: Accelerate

The average arbitrage yield for the most recent ten mergers is 11.5%, representing a 650 bps premium to the yield on cash. In addition, arbitrage yields of 8% to 9% for low-risk mergers are also quite appealing, in our humble opinion, given their high probability of completion and without substantial delays. Nonetheless, I have not heard an arbitrageur complain that spreads are too tight in quite a while.

However, while the current consolidation wave offers many attractive arbitrage opportunities, risks do abound. For example, the current global antitrust environment is generally unfriendly to investors. Some of the antitrust regulators’ moves against high-profile mergers have been head-scratching and somewhat disconcerting.

Lina Khan’s appointment as Federal Trade Commission (FTC) chair in June 2021 brought significant attention to her unorthodox views on antitrust and regulation. As the head of the FTC, Khan has been an influential figure in shaping the agency’s current approach to competition and consumer protection, which has significant effects on the merger market.

One aspect of Khan’s tenure that many perceive as unfriendly to investors is her inclination toward challenging and scrutinizing large companies and their market dominance, specifically in the technology sector. She is against large companies making acquisitions in general, and anti-big tech in particular, and makes no qualms about it.

Since most mergers require antitrust clearance in the U.S. and often additional jurisdictions, close monitoring of agency viewpoints and actions is essential.

Some of the FTC’s recent merger challenges have surprised investors with some farfetched approaches to antitrust enforcement. For example, the agency challenged Amgen’s acquisition of Horizon Therapeutics this month, citing an extremely novel theory of competitive harm that quite frankly has near zero relation to current antitrust law. Thankfully, the FTC must defend its merger challenge in court, and the agency is widely expected to lose (or settle), allowing the parties to consummate the merger. Nonetheless, these baseless merger challenges do introduce unnecessary volatility into market prices and frustrating delays, which can reduce arbitrage returns.

In addition to some puzzling FTC actions, there was a recent perplexing antitrust decision across the pond.

Before Brexit, which has been an unmitigated disaster on all fronts, the European Commission (EC) held authority over competition matters in the U.K. as part of the E.U.’s competition policy framework.

As a member of the E.U., the U.K. adhered to E.U. competition laws and regulations, which the European Commission enforced. However, with the implementation of Brexit, the U.K. established its own competition authority, the U.K. Competition and Markets Authority (CMA), to ensure the effective enforcement of competition and consumer protection laws within its jurisdiction.

Post-Brexit, the CMA operates independently from E.U. competition authorities, including the European Commission. Large corporate mergers now require clearance from the EC (27 member states) and CMA (United Kingdom).

Any large merger, even between American companies, will require approval from the FTC (of the Department of Justice) in the U.S., along with the U.K. CMA and the European Commission. Microsoft’s $68 billion acquisition of video game developer Activision Blizzard fits the bill as a “large merger”, and therefore requires approval from several antitrust regulators around the globe.

This acquisition is classified as a vertical merger, in which a platform (Microsoft’s Xbox) seeks to acquire a company downstream — a firm that develops games for its platform. Historically, vertical mergers have passed antitrust muster relatively easily, given the lack of horizontal overlap and its unlikely effect on consumer prices.

Oddly, last month, the UK CMA chose to block the Activision acquisition, citing potential competitive harms in the nascent cloud gaming market, which does not quite exist yet in substantive form. What makes the situation stranger is that the CMA’s big brother, the European Commission, found the deal to be pro-competitive in the cloud market (given the remedies offered). Two related agencies came to opposite conclusions on the merger, which is confusing even to the most talented arbitrageurs. In any event, it is clear to all market participants that the UK CMA made an error in its decision to block the merger, especially after the EC came to the opposite conclusion. The facts are supportive of the European Commission’s clearance of the deal.

In any event, both Microsoft and Amgen have vowed to press on, aiming to defeat the regulators’ challenge of their acquisitions. It is likely that both will be successful, and close their respective acquisitions, albeit with significant delay and elevated volatility.

There are several concepts that an arbitrageur must take into account when structuring a portfolio in the current market environment:

- Large-cap M&A faces an elevated risk of facing difficulties from regulators, even if on paper the transactions present no competitive concerns.

- Given the potential higher frequency of merger challenges from antitrust agencies, large deals will be delayed. An arbitrageur must demand a higher yield to account for the likelihood of a merger taking longer to close.

- More turbulence from government agencies will cause greater volatility in merger spreads. Arbitrageurs must have increased flexibility to capitalize on the higher variability in spreads across a deal cycle, with the ability to trade around decisions, setbacks, and successes.

Regardless, the current wave of consolidation in public markets is picking up steam, presenting a wide array of investment opportunities in merger arbitrage, despite some potential risks. As a result, attractive arbitrage yields abound, but allocators need to be cautious and informed in order to generate the highest risk-adjusted returns.

With the average merger arbitrage yield north of 10%, there’s no need to sell in May when you can capitalize on M&A.

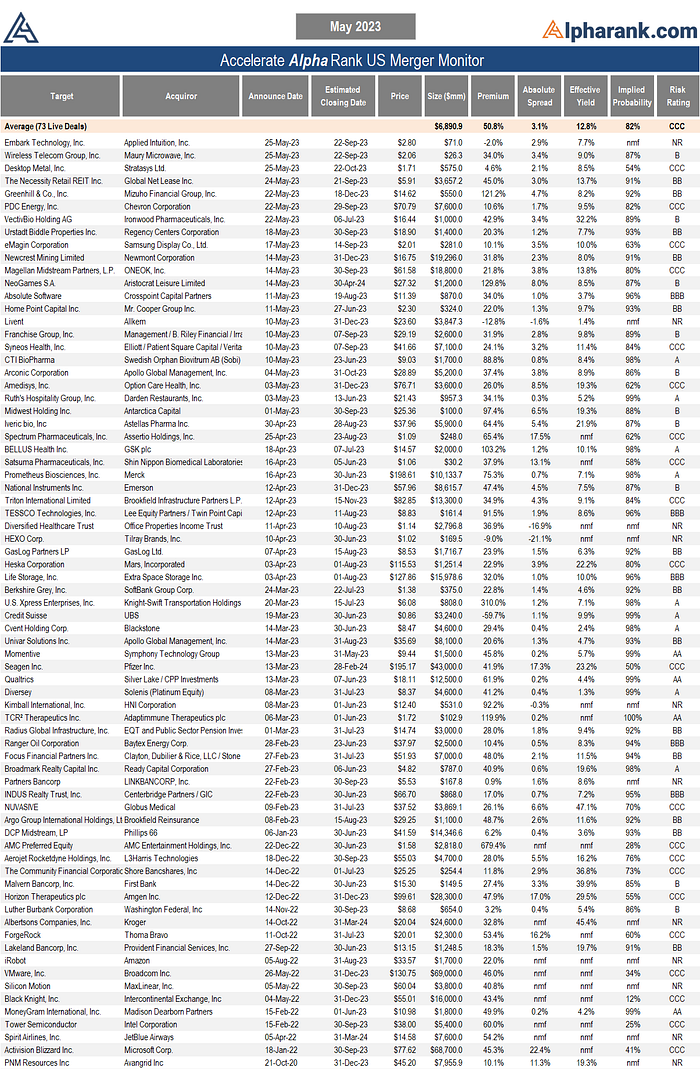

The AlphaRank.com Merger Monitor below represents Accelerate’s proprietary analytics database on all announced liquid U.S. mergers. The AlphaRank Merger Arbitrage Effective Yield represents the average annualized returns of all outstanding merger arbitrage spreads and is typically viewed as an alternative to fixed income yield.

Each individual merger is assigned a risk rating:

- AA — a merger arbitrage rated ‘AA’ has the highest rating assigned by AlphaRank. The merger has the highest probability of closing.

- A — a merger arbitrage rated ‘A’ differs from the highest-rated mergers only by a small degree. The merger has a very high probability of closing.

- BBB — a merger arbitrage rated ‘BBB’ is of investment grade and has a high probability of closing.

- BB — a merger arbitrage rated ‘BB’ is somewhat speculative in nature and has a greater than 90% probability of closing.

- B — a merger arbitrage rated ‘B’ is speculative in nature and has a greater than 85% probability of closing.

- CCC — a merger arbitrage rated ‘CCC’ is very speculative in nature. The merger is subject to certain conditions that may not be satisfied.

- NR — a merger-rated NR is trading either at a premium to the implied consideration or a discount to the unaffected price.

The AlphaRank merger analytics database is utilized in running the Accelerate Arbitrage Fund (TSX: ARB), which may have positions in some of the securities mentioned.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). Visit Alpharank.com for more information. Disclaimer: This research does not constitute investment, legal or tax advice. Data provided in this research should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this research is based on current market conditions and may fluctuate and change in the future. No representation or warranty, expressed or implied, is made on behalf of Accelerate as to the accuracy or completeness of the information contained herein. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Accelerate may have positions in securities mentioned. Past performance is not indicative of future results.